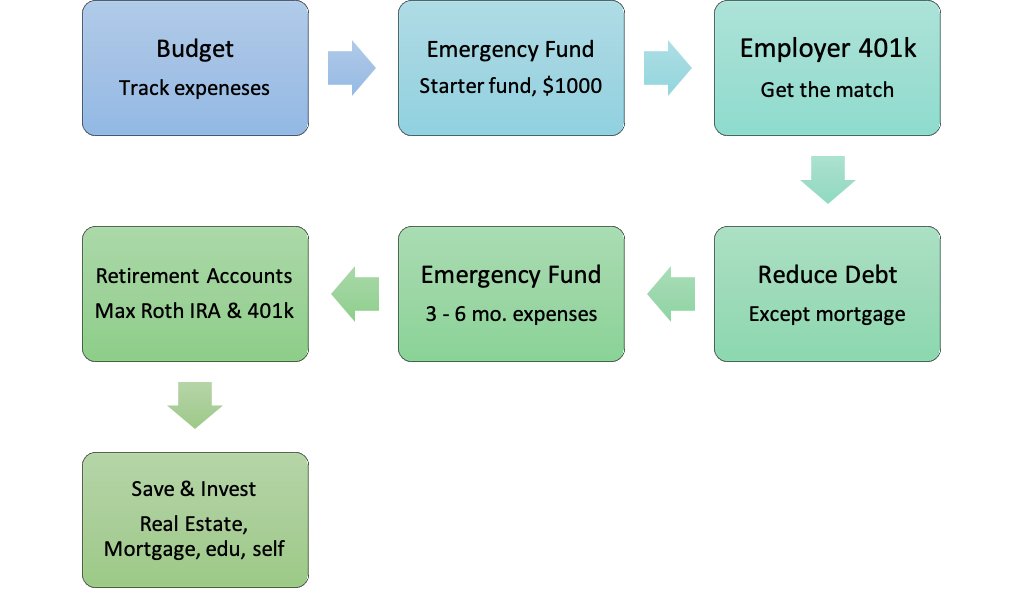

Should we save our money or pay off debt? What about retirement accounts?

If you have ever had these questions, you are not alone. The 7 steps below are a general guide that will help you along your financial journey and point you in the right direction.

1. Create a Budget aka Cash Flow

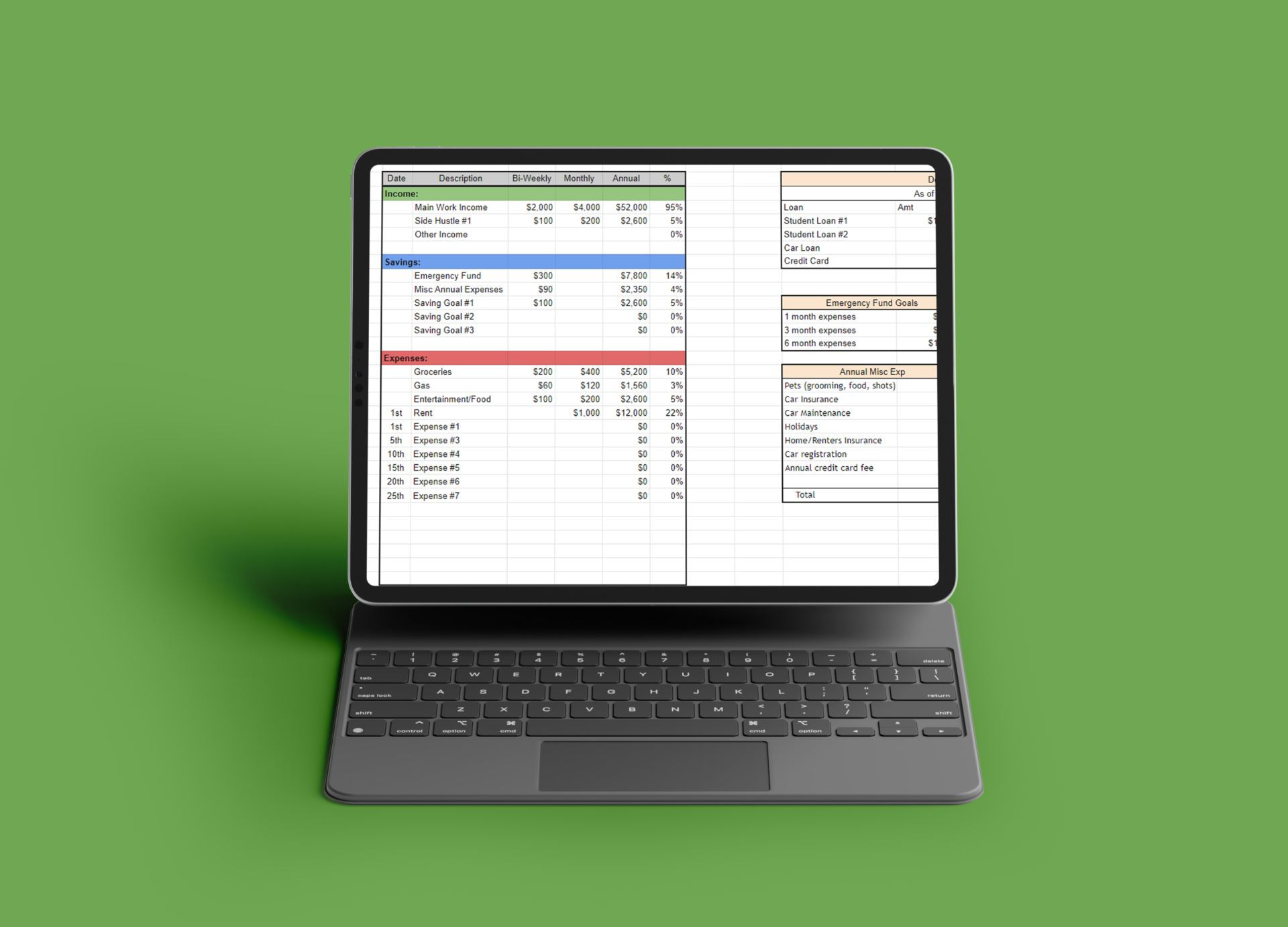

Creating a budget is the first step in taking control of your finances. Now some people get caught up with the word “budget” and see it as scarcity. Simply think of it as a cash flow statement. You want to see what money is coming in and going out. Understanding where all your money is going is number one. Once I started tracking my expenses I was shocked at how much money I was spending on eating out for lunch every day. Once you realize where all your money is going you can easily see places where you can improve.

A few different ways to track your cash flow are finance apps or excel. I use a mix of both. I recently downloaded an app to track my spending. There are a lot of good ones out there, use what works best for you. Both of these together help give me a clear snapshot of my finances. Get started today by using the excel template on the home page.

What has helped me the most is a bi-weekly or paycheck budget method. Monthly budget methods always seemed weird to me since the majority of people get paid bi-weekly and on different dates each month. I also use a zero-sum budget where I give every single dollar a category. This could be food/drinks out, emergency funds, gas, student loans, etc.

2. Starter Emergency Fund

The financial goal most people struggle with is getting out of debt. If you create an emergency fund or a rainy day fund this will create a buffer from you taking on more debt.

According to a Forbes article, 63% of people cannot cover a $500 unexpected expense. Dave Ramsey suggests – start by saving $1,000 as a baby step. I 100% agree with him. This is a good starting point, especially if you don’t have an emergency fund at all. Some people are going to say this is not enough but this will cover most surprises that life throws at you. And before this, you most likely didn’t have $1000 saved up. So start here.

What worked for me was creating a separate savings account at a different bank and having money automatically withdrawn from my paycheck before I even saw it. If you keep this money separate you will be less tempted to spend it. Creating a barrier at a different bank will also make it a little more difficult to transfer into your main checking account. Some banks will allow you to create a nickname so if you try to withdraw from it you will see it is for your emergency fund and most likely think twice about spending it. This will help to prioritize your money. I recommend using Ally Bank for your Emergency fund.

3. Take the Employer Match

Most employers offer a company retirement plan, the most common is a 401k. Often times they offer an employee match to get you to sign up.

If possible, always take the employer match from your company. This is a 100% return on your retirement investment. Almost no other investment will give you this return. It may not seem like a lot right now, but this will grow exponentially with compound interest.

Do not contemplate too much trying to figure out all the different funds in your workplace 401k plan. Simply pick a target-date fund and move on. It will show different years at the end of the fund name and you just want to pick your retirement date. It picks stocks and bonds ratios based on your retirement date. The younger you are the higher the stock to bond ratio. As you get older it lowers the stocks and increases in bonds to preserve wealth. This is what I currently have through my work 401k plan. Have the 4% (or whatever percentage they match) automatically come out of your paycheck so you don’t have to think about it. Let it grow over time and when you are about to retire you will have a good-sized stack of money in there.

It doesn’t matter too much if you chose pretax or post-tax for the 401k. I choose a post-tax 401k since I am young and most likely at the lowest tax bracket I will be at. Also, no one can predict what taxes will be like in 20-30 years. It’s good to diversify and have some pretax retirement accounts and some post-tax.

4. Pay off All Debt Except Mortgage

This next step is to become debt-free except for a mortgage payment if you have one.

Below are 2 approaches that are tried and true to work for paying off debt.

The debt snowball method:

This has you list your debt in order from the smallest loan to largest. You pay the minimum payment on each one except the smallest loan. You throw all your extra money towards that small loan until it’s paid off. Then you take what you were paying on the small loan and put that towards the next smallest loan until you’re debt-free. This uses small wins to keep you motivated and encouraged to keep paying down debt. Money is all psychological so small victories are crucial to keeping us on the right path.

The debt avalanche method:

This has you list your debt in order from the highest interest rate to the lowest interest rate. This method will save you the most money in interest. However, the first loan could be a large amount so you will not be able to see those small wins like the debt snowball method. If you do not need those small victories to keep you going, then this is the best approach to saving the most money in interest.

I like to use a hybrid of the two methods. If you have any crazy high-interest rates over 10%, such as credit cards, prioritize these debts first. Then focus on the loans with the smallest balance to get your small wins to keep you going. If you have a credit card with 25% interest you have to pay this off first or you will be paying on it forever. Compound interest will work against you. Not good.

5. Emergency Fund of 3 to 6 Months

Congrats, you are now debt-free. *Pop a few bottles, and pat yourself on the back*

Now it’s time to beef up your emergency fund. A 3-month emergency fund to cover your necessities will be perfect for most people. Some people like to play it safe and shoot for 6 months or even a year. It all depends on what makes you feel secure.

Take your current monthly expenses and multiply them by 3 or 6. This is your emergency fund goal.

Like I mentioned above, the best way is to have an amount of money automatically taken out of your check and put into your emergency fund. Don’t wait to see what you have leftover at the end of the month to put into your emergency fund.

Pay yourself first!

6. Increasing Retirement Contributions: Roth IRA & 401k

Now that you have an emergency fund this will relieve a good majority of your financial worries.

Time to invest some more money into your retirement accounts and grow your wealth. It’s time to open another investment retirement account – your Roth IRA. This may be one of the best retirement tools out there. Whenever you see the word “Roth” it means after tax. After taxes come out of your money you will then invest it in a Roth IRA. It will grow and since it is a retirement account you will not have to pay taxes when you pull the money out at 59 1/2. Another perk of this account is that whatever contributions you made to the account you can take out without penalty.

BUT only the contributions.

I would not recommend doing this because you want to save this for your retirement and get the effects of compound interest on your money.

After you max out your Roth IRA, which in 2022 is capped at $6,000 per year – you can contribute more to your 401k if you would like. If you are on your path to financial independence, you will want to start maxing out your 401k through your workplace retirement plan. This has an annual cap of $20,500 in 2022.

The Roth IRA is just the account, you still must select the funds you want to invest your money in.

This is very important! I read an article that mentioned a person had money automatically withdrawn into their Roth IRA, but after 20 years did not invest in any funds. It just sat in the account as a savings account. Make sure to invest your Roth IRA!

Where to invest?

To keep things simple just pick a target date fund for both your Roth IRA and 401k through work. Most people do not know where to get started with investing and end up having decision paralysis. There are way too many funds to pick from. Pick your target-date fund and move on with your life.

There are many places to open a Roth IRA account. I suggest Vanguard, Fidelity, or Schwab. They are all very reputable. I use Fidelity. That doesn’t mean it’s the best, it’s just what I use.

7. Set Up Other Investments

At this point, you are set and you will be wealthy.

If you have extra money to invest, there are some good options out there.

In no particular order below:

- Invest in yourself – go back to school, take a class, etc.

- Save for your kid’s college

- Invest in a taxable brokerage account – Vanguard, Fidelity, Schwab

- Pay off your mortgage if you have one

- Invest in real estate – rental properties, Airbnb, flipping houses

I understand you aren’t going to be able to complete all 7 of these steps in a month or even a year. However, this gives you a good financial roadmap. If you follow the actions above, you will be greatly ahead of the majority of people.

Live within your means and be intentional with your money.

What steps have you taken in your personal finance journey?